Biology Becomes Code

In June 2025, a small paper appeared in Nature Medicine that most investors completely missed.

A drug called rentosertib had just completed Phase IIa clinical trials for idiopathic pulmonary fibrosis — a devastating lung disease that kills most patients within five years of diagnosis. The results were remarkable: patients on the highest dose saw their lung function improve by 98.4 mL, while the placebo group declined by 20.3 mL.

That’s not the interesting part.

The interesting part is how this drug was created.

Both the disease target and the molecule itself were discovered and designed entirely by artificial intelligence. No human chemist sat at a bench and intuited the compound. No team spent a decade screening millions of molecules in a laboratory. An AI platform called Pharma.AI identified a novel protein target called TNIK that nobody had previously linked to lung fibrosis, then designed a molecule from scratch to inhibit it.

From project start to preclinical candidate: 18 months. From target discovery to Phase I: under 30 months. Total molecules synthesized and tested: roughly 80.

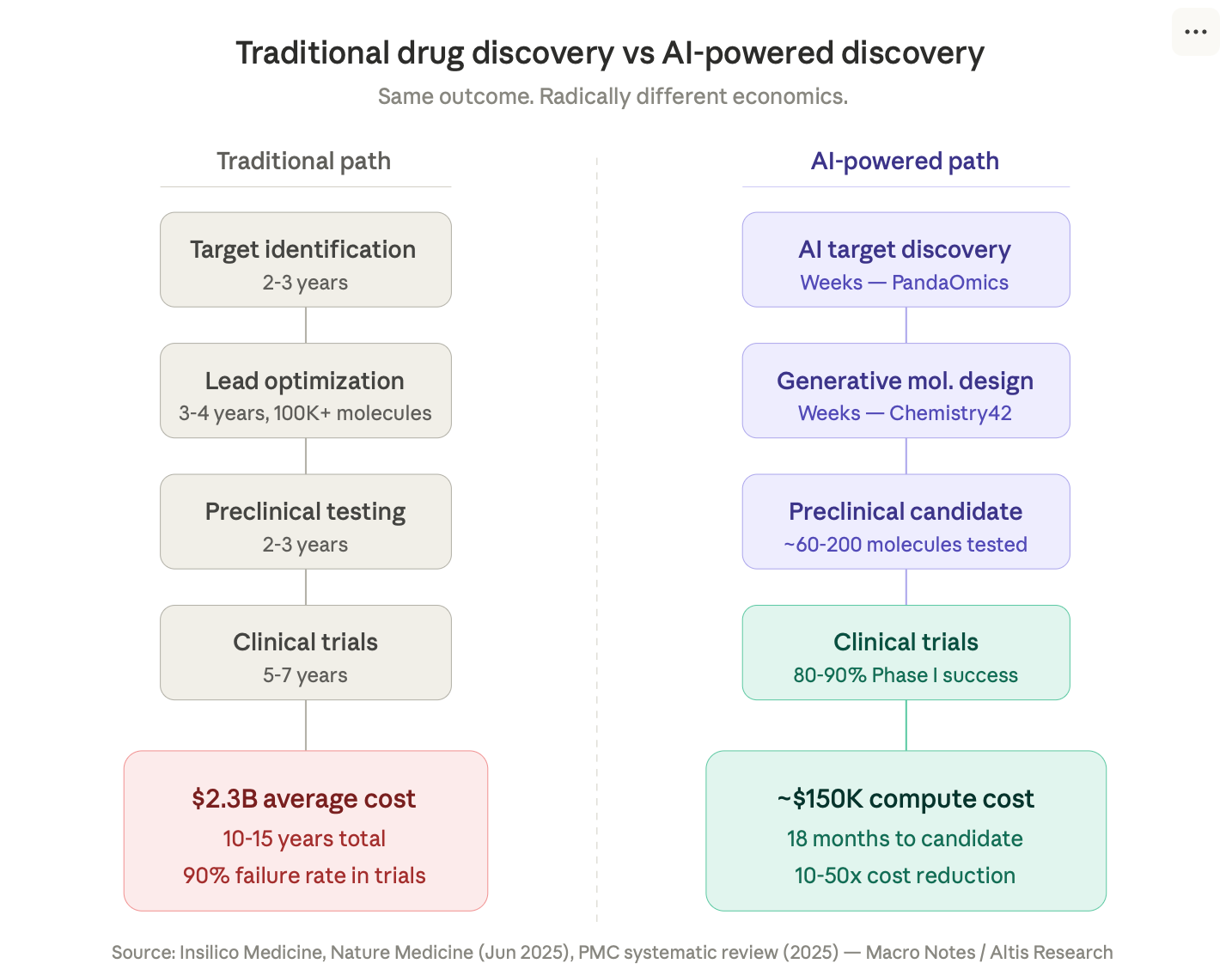

For context, traditional drug discovery takes 10 to 15 years, costs over $2 billion, requires screening hundreds of thousands of molecules, and fails 90% of the time in clinical trials.

Alex Zhavoronkov, the CEO of Insilico Medicine — the company behind rentosertib — called it “the most important result in my life to date.” He’d expected the drug to be safe. He did not expect to see a clear dose-dependent efficacy signal after just 12 weeks.

I read that paper three times. Then I started pulling every thread I could find on what’s happening at the intersection of AI and biology.

What I found changed my entire view of where the next decade of outsized returns will come from.

The $2 Billion Problem

Here’s a number that should bother every investor in healthcare: $2.3 billion.

That’s the average cost to bring a single drug from initial discovery to pharmacy shelf. The process takes over a decade. And after all that money and time, nine out of ten drug candidates that enter clinical trials will fail.

This has been the economic reality of pharmaceutical R&D for fifty years. It’s why drug prices are astronomical. It’s why rare diseases go untreated. It’s why the biggest pharma companies in the world spend more on marketing than on research — because research is a casino where the house almost always wins.

But something changed.

In 2021, Insilico Medicine nominated rentosertib as a preclinical candidate for $150,000 in computational costs. Not $150 million. One hundred and fifty thousand dollars.

The entire journey — from AI identifying a novel target that no human had found, to designing a molecule to hit it, to getting that molecule into human trials — cost a fraction of what a single failed Phase I study costs at a traditional pharma company.

And Insilico isn’t alone.

Exscientia, a UK-based company, became the first to put an AI-designed molecule into human trials back in 2020. They did it in 12 months. The industry average at that time was four and a half years for the same stage.

Schrödinger, which takes a physics-based approach rather than pure machine learning, saw its compound zasocitinib advance all the way to Phase III through a partnership with Takeda. In December 2025, Takeda reported that the AI-designed molecule successfully treated plaque psoriasis in two late-stage trials.

As of early 2026, more than 173 AI-discovered drug programs are in clinical development worldwide. That number was essentially zero five years ago.

Something fundamental is shifting. And the market hasn’t priced it in.

The Moment Biology Became an Engineering Discipline

To understand why this matters so much, you need to understand what actually changed.

For all of human history, drug discovery has been an artisanal discipline. A brilliant scientist has an intuition about a biological mechanism. A team of chemists painstakingly designs molecules by hand, one at a time, testing each in a lab to see if it works. Most don’t. The few that do get tested in animals, then in humans, over years and years — and most still fail.

It’s the equivalent of designing a car by randomly welding metal pieces together and seeing if the engine starts.

What AI does is fundamentally different. It doesn’t guess. It predicts.

Insilico’s platform, Pharma.AI, works in three stages. First, an engine called PandaOmics analyzes millions of datasets — genomic data, clinical records, research papers, patents — to identify disease targets that humans might never find. It was PandaOmics that flagged TNIK as a promising target for fibrosis, a connection that wasn’t in the existing medical literature.

Then a generative chemistry engine called Chemistry42 designs molecules optimized for that target. It uses over 500 predictive models — transformers, GANs, reinforcement learning — that reward and punish generated molecules based on their predicted properties: potency, selectivity, toxicity, how they’re absorbed and metabolized by the body.

From project initiation to preclinical candidate nomination, Insilico’s 22 drug programs between 2021 and 2024 averaged 12 to 18 months each, requiring synthesis of only 60 to 200 molecules per program.

Traditional pharma screens 10,000 to 100,000 molecules per program. Over 4 to 6 years. At exponentially higher cost.

This isn’t an incremental improvement. It’s a phase transition. Biology is crossing from artisanal craft to predictive engineering — the same shift that happened when software ate media, when algorithms ate finance, when machine learning ate advertising.

The implications are enormous.

The Arms Race Has Started

The smart money is already moving — fast.

Isomorphic Labs, the drug discovery arm of Google DeepMind (yes, the team that won the Nobel Prize for AlphaFold), signed nearly $3 billion in partnerships with Eli Lilly and Novartis in early 2024. Lilly paid $45 million upfront with up to $1.7 billion in milestone payments. Novartis paid $37.5 million upfront with up to $1.2 billion in milestones. Novartis then doubled its commitment in early 2025.

These aren’t speculative bets. These are the two largest pharma companies on earth paying billions to access AI capabilities they cannot build internally — specifically to go after “undruggable” targets that traditional methods can’t reach.

Recursion Pharmaceuticals merged with Exscientia in mid-2025, creating the largest AI-native drug discovery platform in the world. The combined entity has over 10 clinical programs, partnerships with Roche, Sanofi, Bayer, and Merck KGaA, and more than $20 billion in potential milestone payments. Their “Recursion OS” is a closed-loop system where robots run experiments, AI analyzes results, predicts next steps, and triggers new experiments — 24 hours a day, 7 days a week, with no human in the loop.

Sanofi signed a $1.2 billion collaboration with Exscientia (before the merger) to discover up to 15 novel molecules in oncology and immunology. AstraZeneca signed a $247 million deal with Absci to develop an AI-designed antibody for cancer.

And then there are the self-driving labs.

NVIDIA launched BioNeMo, a platform that gives drug discovery companies access to GPU-accelerated models for molecular simulation. Companies like Multiply Labs are building robotic digital twins of their labs using NVIDIA’s Isaac Sim framework — testing experiments virtually before running them physically. Opentrons is training lab robots with AI so they can operate beyond constrained environments.

The vision these companies share is audacious: fully autonomous drug discovery, where AI designs the experiment, robots execute it, AI analyzes the results, and the cycle repeats — compressing years of work into weeks.

We’re not there yet. But the trajectory is undeniable.

The Numbers That Matter

Let me give you the data that frames the investment thesis.

The market is massive and growing fast. The global synthetic biology market was valued at $17 billion in 2025 and is projected to reach $95 billion by 2034 — a compound annual growth rate of 21%. The AI drug discovery market specifically is growing at 40%+ CAGR.

AI drugs are outperforming traditional drugs — early evidence. AI-discovered compounds are achieving 80 to 90 percent success rates in Phase I trials, compared to the historical average of roughly 52%. This is the single most important data point in the entire sector. If that differential holds through later stages, it fundamentally changes the economics of pharma R&D.

The pipeline is exploding. 173+ AI-discovered programs in clinical development as of early 2026. Roughly 94 in Phase I, 56 in Phase II, 15 in Phase III. Fifteen to twenty programs are expected to enter pivotal trials this year.

The first FDA approval could come in 2026 or 2027. Analysts estimate roughly a 60% probability. The most advanced candidates are rentosertib (Insilico Medicine, Phase IIa complete, Phase IIb discussions ongoing) and zasocitinib (Schrödinger/Takeda, Phase III with positive data).

The cost compression is staggering. Insilico’s computational costs for rentosertib: $150,000. Traditional drug discovery for the same stage: $300-500 million. Even accounting for wet lab validation, the cost reduction is 10-50x.

Big pharma is all in. Cumulative deal value for AI drug partnerships exceeds $15 billion. In 2023 alone, AI-driven biotech startups raised over $4.5 billion in venture capital.

And here’s the contrarian part: the public market hasn’t repriced any of this.

Recursion (RXRX) trades at roughly $1.8 billion in market cap with $509 million in cash, $20 billion in potential milestone payments from partners, and 10+ clinical programs. Schrödinger (SDGR) trades at $1.8-2.2 billion with $180-200 million in revenue, growing, and a Phase III asset through Takeda. Relay Therapeutics (RLAY) is executing a focused oncology strategy with a differentiated AI platform that models protein motion — something no other platform does.

The market is pricing these companies as speculative biotech. They’re not. They’re platform companies building the operating system for 21st-century drug discovery. The analogy isn’t “another biotech with a pipeline.” The analogy is Palantir in the early days of government data analytics, or Veeva when it was first replacing legacy CRM in pharma. Horizontal platforms that become the infrastructure layer of an entire industry.

Why I’m Building a Position Now

Here’s my framework.

We’re at the exact inflection point where AI drug discovery transitions from “interesting technology” to “validated paradigm.” The first Phase IIa success has been published in Nature Medicine. Phase III trials are reading out in 2026. The FDA published its first guidance on AI in drug development in January 2025, with final guidance expected Q2 2026.

Every major pharma company on earth is now signing AI partnerships — not as R&D experiments, but as core pipeline strategy. Lilly, Novartis, Roche, Sanofi, AstraZeneca, Bayer, Merck KGaA, Takeda. The question is no longer “will AI work in drug discovery?” It’s “which AI platforms will capture the most value?”

I’ve seen this pattern before. In 2024, I was writing about copper miners and uranium producers before the market caught on. The infrastructure bottleneck thesis. The “invisible monopoly” framework. Find the companies that are essential to a structural shift, buy them before the market reprices, and hold through the noise.

AI drug discovery is the same pattern. The structural shift is the compression of drug development timelines from decades to months. The invisible monopoly is the proprietary data and closed-loop learning systems that these platforms are building — every experiment makes the AI smarter, every partnership adds data, every clinical trial validates the platform. The moats deepen with time.

The catalysts are clear. First FDA approval of an AI-designed drug. Phase III readouts. New mega-partnerships. And the moment the market realizes that these aren’t biotech lottery tickets — they’re the next generation of pharmaceutical infrastructure.

What follows is the premium section: my complete playbook for this thesis — specific positions, entry zones, position sizing, catalyst timelines, and strategies for accessing private companies like Isomorphic Labs.