The $200 Billion Slow-Atom Problem

There are about forty companies on the planet right now racing to build the next generation of nuclear reactors.

There are four facilities in the entire Western world that can enrich the uranium to fuel them.

You’ve heard of all forty reactor companies.

You’ve heard of none of the four.

That gap is what this letter is about.

It’s also, I think, one of the more interesting industrial stories happening anywhere in the world right now — and one of the least understood by the equity market that will eventually have to price it.

Over the next several thousand words I want to do three things.

First, walk you through how a nuclear reactor actually works — not in textbook abstraction, but in a way that lets you understand why the current wave of advanced reactors is genuinely different from what came before.

Second, explain what nuclear fuel really is, why it’s harder to make than most people realize, and why the constraint isn’t where the headlines say it is.

Third, lay out the structural mismatch — somewhere in the neighborhood of $200 billion of capital that needs to flow into a forgotten part of the energy economy over the next ten years — and the historical pattern that, in my view, makes this one of the most asymmetric setups in industrial equities today.

I’ll get to the names. I’ll also tell you what I don’t like, and where this thesis could be wrong.

But first: the atoms.

Before we continue, here’s a sponsored message from our partner DataToBrief. If you’d like to sponsor the newsletter as well, feel free to reach out at pierre@altis.finance

A handful of funds in the US and Europe are quietly replacing junior analyst work with autonomous AI agents.

We just published a whitepaper that breaks down what these systems actually do, where they add edge versus where they fail, how the early adopters are integrating them into their process, and what the next 18 months look like for analysts and PMs.

If you are an allocator, analyst, or PM trying to understand whether this is hype or signal, the whitepaper is written for you.

Free, no signup wall.

The whitepaper is published by DataToBrief, the AI research platform institutional investors use to generate thesis memos, run macro screeners, and monitor active positions.

Thanks to DataToBrief for partnering with us on this edition—don’t forget to visit their site to learn more (it’s a great product and definitely worth a look): https://datatobrief.com. Now let’s get back to the rest of today’s insights.

I. What actually happens inside a reactor

Before we can talk about fuel, we need to be on the same page about what fuel does.

Every nuclear reactor in the world, whether it’s a 1970s pressurized water giant in Pennsylvania or a brand-new small modular design on a Google data center campus, does the same fundamental thing. It splits atoms of uranium. The splitting releases heat. The heat boils water. The steam turns a turbine. The turbine spins a generator. The generator makes electricity.

That’s it. A nuclear plant is, at its core, a very sophisticated kettle.

What makes it sophisticated is what’s happening inside the kettle.

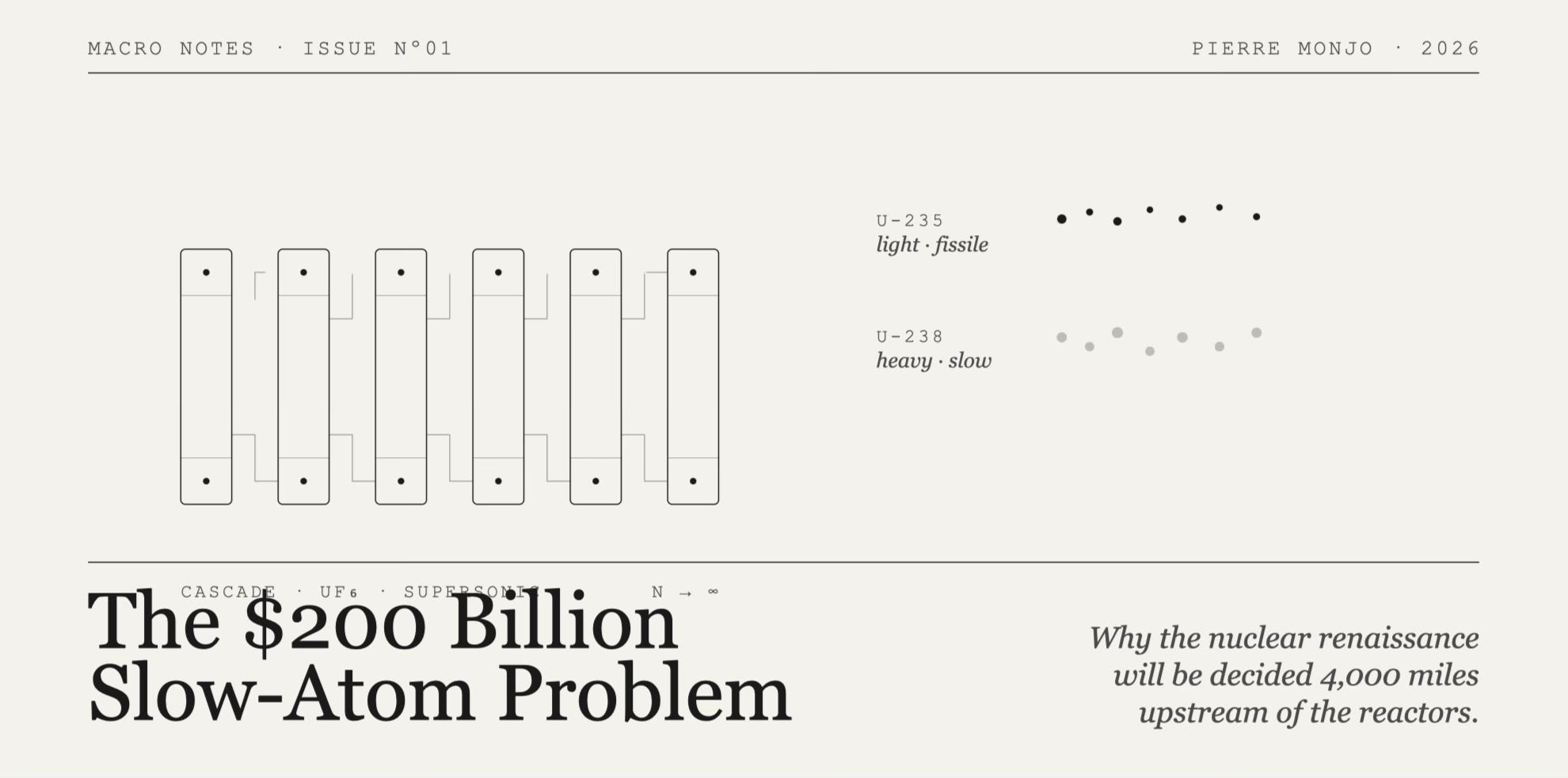

Natural uranium — the stuff you dig out of the ground in Saskatchewan or Kazakhstan — is mostly two isotopes. About 99.3% of it is uranium-238, which is heavy and stable and, for our purposes, useless. About 0.7% of it is uranium-235, which is lighter and, crucially, fissile — meaning that when a neutron hits its nucleus at the right speed, the nucleus splits.

When it splits, three things happen.

First, it releases energy. A lot of energy. One gram of uranium-235, fully fissioned, produces about as much energy as three tonnes of coal.

Second, it releases two or three more neutrons. These fly out at high speed.

Third — and this is the part that turns physics into engineering — those neutrons, if they’re slowed down to the right speed and they hit another U-235 nucleus, cause it to split too. Which releases more neutrons. Which split more atoms. Which releases more neutrons.

That’s a chain reaction. That’s where the heat comes from.

The job of a nuclear reactor, more or less, is to set up the conditions for that chain reaction to happen at a precisely controlled rate. Too slow and the reactor stops. Too fast and you have a serious problem.

There are three things every reactor needs to do this.

It needs fuel — uranium with enough U-235 in it to sustain the chain reaction.

It needs a moderator — something to slow the neutrons down to the right speed. The neutrons that come out of fission are too fast to easily split the next atom. They need to be moderated. In most reactors, this is done with ordinary water. The water bumps against the neutrons, takes some of their energy, and slows them down to what physicists call “thermal” speeds.

And it needs a coolant — something to carry the heat away from the core so the reactor doesn’t melt itself. In most reactors today, this is the same water that does the moderating, which is one of the clever simplifications of the design.

A typical pressurized water reactor — the dominant design in the United States, France, China, and Japan — runs natural uranium that has been enriched to roughly 3-5% U-235. The water serves both functions. The chain reaction is controlled by inserting and withdrawing rods of neutron-absorbing material (typically boron or cadmium) into and out of the core. When you want more power, you pull the rods out. When you want less, you push them back in.

That, in plain language, is a nuclear reactor.

Now we can talk about what’s changing.

II. Why the new reactors are different (and why it matters)

The reactors being built today — the small modular reactors, the advanced reactors, the designs commissioned by Google and Amazon and Microsoft — are different from the existing fleet in several important ways.

They are smaller. A traditional large nuclear plant produces around 1,000 megawatts of electricity. An SMR produces between 50 and 300. A microreactor might produce as little as one or two.

They are modular, which is the second word in their name and the genuinely important one. Rather than being built piece by piece on a single sprawling site over a decade — the way large reactors have always been built — SMRs are designed to be manufactured in a factory and shipped, mostly complete, to where they’ll be used. The promise is faster construction, more predictable cost, and economies of replication rather than economies of scale.

They are designed for different applications. The existing nuclear fleet was built to feed electrical grids. The new fleet is being designed, increasingly, to feed specific buyers — a data center, a chemical plant, a port, a remote community.

And — this is the part most relevant to my story — they run on different fuel.

To understand why, you have to think about what enrichment actually buys you.

Remember that natural uranium is 0.7% U-235. The rest of the cycle — slowing neutrons with a moderator, controlling the rate with absorbing rods, transferring heat with a coolant — is built around the physics of operating with that small fraction of fissile material.

If you enrich the uranium more — say, to 5% U-235 instead of 3.5% — you get more fissile material per kilogram of fuel. The reaction is denser. You can make the core smaller. You can run longer between refuelings. You can simplify some of the engineering that exists, in current reactors, to compensate for the fact that you’re operating with diluted fuel.

If you enrich further — to between 5% and 20% U-235, the range called HALEU, high-assay low-enriched uranium — you can do things with reactor design that simply weren’t possible at lower enrichments.

You can make reactor cores small enough to fit on a truck.

You can run for ten or twenty years between refuelings, instead of eighteen months.

You can use coolants other than water — molten salt, molten lead, helium gas, liquid sodium — which allows the reactor to run at much higher temperatures, which improves thermodynamic efficiency, which means more electricity for the same amount of fuel.

You can build reactor designs where the physics itself prevents a meltdown — where, if something goes wrong and the operators do nothing, the reactor just cools itself down by natural convection. These are called passively safe designs, and they are not a marketing term. They are a real consequence of being able to use denser fuel in smaller cores with more exotic coolants.

To take one example: TerraPower’s Natrium reactor, backed by Bill Gates and ordered by a utility in Wyoming, uses liquid sodium as a coolant instead of water. Sodium has a much higher boiling point than water, which means the reactor can run at around 500°C instead of around 320°C. Higher temperature means more efficient electricity generation. But sodium-cooled reactors only work well with denser fuel. They need HALEU.

Take another: X-energy’s Xe-100, backed by Amazon. It uses helium gas as the coolant and graphite as the moderator, with the fuel packed into small ceramic pebbles. The design is inherently safe — the geometry of the pebbles makes runaway fission physically impossible — but it only works because each pebble contains HALEU-enriched fuel.

Or Oklo’s Aurora — a microreactor designed to run for a decade without refueling, the size of a small house, with no on-site operators required. None of that is possible with conventional 5%-enriched fuel.

This is the trade. The new generation of reactors gets you smaller, safer, cheaper-to-deploy, longer-lasting, and more efficient — but only if you can give them fuel that nobody, outside Russia and China, currently produces at scale.

And that is the part of the story where it stops being about reactors at all.

III. What enrichment actually is

I’ve been throwing the word “enrichment” around. Let’s stop and look at what it physically means.

Uranium atoms come in two main flavors, as we said: U-238 (heavy, useless) and U-235 (light, fissile). Chemically, they are identical. They form the same compounds. They react the same way. The only difference is their mass — U-238 is about 1.25% heavier than U-235.

To separate them, you have to exploit that tiny mass difference. And the way the modern world does it is with a machine called a gas centrifuge.

Here’s the basic picture.

You take your uranium ore concentrate and convert it into a gas called uranium hexafluoride, or UF₆. UF₆ is, in normal life, a solid yellow crystal. Heat it gently and it sublimes into a colorless gas. That gas is your input.

You feed the gas into a tall, narrow metal cylinder — a centrifuge — and spin it. Fast. Astonishingly fast. The outer wall of a modern enrichment centrifuge moves at around 400 to 500 meters per second, which is faster than the speed of sound. The cylinder is mounted on a magnetic bearing at the bottom and a needle bearing at the top, in a near-vacuum chamber, and it spins continuously for years without stopping.

Inside the spinning cylinder, two things happen.

The heavier U-238 atoms get pushed slightly more strongly toward the outer wall.

The lighter U-235 atoms drift slightly more strongly toward the center.

Slightly. We’re talking about a small enrichment per pass — a fraction of a percent. So you don’t run the gas through one centrifuge. You run it through a cascade of them: hundreds, sometimes thousands, connected in series. The gas that comes out of one centrifuge slightly enriched goes into the next, gets enriched a little more, goes into the next, and so on. After thousands of passes, you have a gas stream that is meaningfully enriched in U-235.

You take that gas, convert it back to a solid, machine it into ceramic pellets, stack the pellets inside long thin metal tubes, bundle the tubes into fuel assemblies, and ship them to a reactor.

That, in physical terms, is what enrichment is.

Two things are worth understanding about it.

The first is that the technology is genuinely hard. The centrifuges spin at supersonic speeds for years. The materials science is unforgiving — the rotors have to withstand stresses that would tear ordinary metals apart. The cascades have to be perfectly balanced. The whole system has to be operated under conditions of extreme regulatory scrutiny, because the same machines that enrich uranium to 5% for civilian reactors are, in principle, capable of enriching it to 90% for weapons. Centrifuge enrichment was, for most of the twentieth century, classified technology. There are perhaps a half-dozen countries in the world that have ever successfully built and operated commercial-scale enrichment cascades.

The second is that the unit economics of enrichment are measured in a unit you have probably never heard of, called a separative work unit, or SWU (pronounced “swoo”). A SWU is, very roughly, the amount of work — energy, capital, time — required to separate a given quantity of U-235 from a given quantity of U-238. The U.S. nuclear fleet consumes about 15 million SWUs per year. Russia produces about 28 million SWUs of capacity. All of North America combined produces about 4.3 million.

The mismatch is enormous. And it has consequences we’re about to walk into.

IV. The wrinkle that changes everything

Here is where the picture gets uncomfortable.

The Western enrichment infrastructure I just described — the cascades, the centrifuges, the SWU capacity, the regulatory expertise — was built, over forty years, to produce one specification of fuel: low-enriched uranium, 3-5% U-235, for the existing reactor fleet.

That fleet still exists. It still consumes fuel. It still needs to be served.

But none of the equipment, almost none of the supply chain, was built to produce HALEU. The cascades that enrich to 5% are not configured to enrich to 20%. The transport casks are not certified for the higher fissile densities. The fuel fabrication lines are not equipped to handle the denser material. The regulatory regimes have not been written.

And the only country in the world that currently produces HALEU at commercial scale is Russia.

Let me put a number on what this means.

In June 2025, Centrus Energy delivered 900 kilograms of HALEU to the U.S. Department of Energy. That delivery completed Phase II of a contract that had been signed in 2019.

Six years of work. Less than one metric tonne of fuel.

A single Oklo Aurora reactor, fueled and operating, needs between one and two metric tonnes of HALEU.

The U.S. Department of Energy has projected national HALEU demand at more than 40 metric tonnes per year by 2030, scaling to roughly 50 metric tonnes per year by 2035.

Forty metric tonnes by 2030.

Current Western annual production: under one metric tonne.

If you sit with that gap for a moment — forty times what the entire Western supply chain currently produces, needed within five years — you start to see the shape of what I mean by the slow-atom problem.

It is not a supply shortage. It is a supply void.

The infrastructure to fill it has not yet been built. Some of it has not yet been designed. Several of the companies that will eventually fill it do not yet exist as commercial entities. The TerraPower Natrium project in Wyoming, the X-energy Xe-100 project in Washington state, the Kairos demonstration project for Google in Tennessee — all of them have publicly disclosed that their schedules are now dependent, in part, on fuel availability.

The reactors are designed.

The fuel is not.

V. Why this matters now

I’ve been walking you through physics and industrial history. Let’s now talk about what’s happening in real time, because the consequences are already showing up in unusual places.

Item one. In the eighteen months between October 2024 and today, four of the largest companies on Earth — Microsoft, Google, Amazon, and Meta — have collectively signed more than ten gigawatts of new U.S. nuclear power purchase agreements.

Ten gigawatts is, roughly, the entire installed nuclear fleet of Spain.

The buyers are not utilities. They are hyperscale cloud providers, racing to lock in 24/7 baseload power for AI data centers before the supply gets tighter. Microsoft is restarting Three Mile Island Unit 1. Amazon is converting Susquehanna into a nuclear-powered AI campus and has separately committed up to five gigawatts of X-energy SMR capacity. Google has signed the first corporate SMR purchase agreement in history, with Kairos Power. Meta has signed 1.1 gigawatts with Constellation and issued an open RFP for an additional one to four gigawatts of new nuclear.

The International Energy Agency now projects that global data center electricity use will more than double by 2030, to roughly 945 terawatt-hours — about the present annual consumption of Japan.

Item two. In August 2024, the United States legally banned imports of Russian enriched uranium. Limited waivers can be granted only through January 1, 2028. After that date, the 20% of U.S. nuclear fuel supply that currently comes from Russia is, by law, gone.

There are 94 operating commercial reactors in the United States. They cannot simply switch off.

Item three. Separative work unit prices — the standard measure of enrichment effort — reached $160 in 2024. In 2020 they were $40.

That is a 400% increase in three years, in a commodity that most equity investors have never even heard of, in an industry that the financial press still treats as a sleepy utility category.

Markets do not move four hundred percent in three years for sentimental reasons.

Item four. In January 2026, the U.S. Department of Energy committed $2.7 billion to rebuild American enrichment capacity. The money was split into three roughly equal awards: $900 million to Centrus Energy’s American Centrifuge Operating subsidiary, $900 million to a stealth-mode startup called General Matter (operating at the former Paducah Gaseous Diffusion Plant in Kentucky), and $900 million to Orano Federal Services. An additional $28 million was awarded to Global Laser Enrichment for next-generation laser-based enrichment technology.

That $2.7 billion is on top of Centrus’s own multi-billion-dollar private capital raise. It is on top of a separate $5 billion Orano facility under development in Tennessee, called Project IKE. It is on top of the United Kingdom’s £300 million HALEU allocation. It is on top of European consortium funding for parallel enrichment expansions. It is on top of Korea Hydro & Nuclear Power signing forward supply contracts for fuel from a U.S. facility that has not yet been built.

Add these flows up. Add the utility offtake contracts. Add the implicit valuation of Westinghouse — more on that in a moment. Add the parallel rebuilds in Japan, Korea, and Eastern Europe. Add the downstream investment in fabrication, transport, and storage.

Somewhere in the neighborhood of $200 billion of Western capital expenditure has to flow into the rebuilding of a fuel cycle that decayed for forty years, on a timeline of roughly one decade.

This number is not a wild estimate. It is the agglomeration of publicly announced government programs, private capex commitments, utility purchase contracts, and the visible construction pipeline. If anything, I think it understates the eventual total.

That is what I mean by the slow-atom problem.

Two hundred billion dollars, slowly walking through Ohio, Tennessee, Kentucky, New Mexico, Oxfordshire, Normandy, and Tricastin — building the centrifuges, the conversion lines, the fabrication halls, the transport casks that the world forgot it would need.

The equity market has not yet figured out where to express this.

That is the gap.

VI. The Pentagon-sized building

I want to spend a moment in a specific place, because abstractions are easier to feel when you can picture them.

About sixty miles south of Columbus, Ohio, sits a former Cold War uranium complex called Piketon. Inside the complex is a building roughly the size of the Pentagon. It was built in the 1950s. It was decommissioned in 2013.

It is currently being woken back up.

Inside, in a high-ceilinged industrial hall, rows of tall grey cylinders — centrifuges — each spin a column of UF₆ gas at supersonic speeds. The cylinders themselves are not photogenic. They look like industrial water heaters in a steel cathedral. There is no observation deck. There are no rendered visualizations. There is no charismatic founder doing the conference circuit.

There is, however, the only first-of-a-kind HALEU production cascade in the United States.

The building is operated by Centrus Energy, ticker LEU on the New York Stock Exchange — a company most equity investors have never heard of, and which a year ago was trading at a fraction of where it sits today.

The point of bringing you to Piketon is not to romanticize a building. It’s to make a single observation.

The room where the future of nuclear power will actually be decided does not look like the room you’ve been reading about. It looks like an industrial hall in southern Ohio.

The room you’ve been reading about — the one with the rendering of a small modular reactor next to a data center in 2032 — does not yet exist.

The room in Piketon does.

Both rooms matter. But only one of them is operating today.

VII. The historical pattern

A careful reader at this point reasonably asks: “okay, but is this just a moment? Is it just a price spike that mean-reverts once new capacity comes online?”

Fair question. And the honest answer is: I don’t think so — and history suggests we shouldn’t. Cycles like this rhyme more than they vary, and I want to spend a moment on three earlier ones, because once you’ve seen the pattern, you start to see it everywhere.

The U.S. shale boom, 2008-2014.

If you remember this period as an equity story, you probably remember the upstream — the drillers. Pioneer Natural Resources, Continental, Chesapeake, EOG. The great proliferation of independents drilling the Bakken, the Eagle Ford, the Permian. The headlines were about the resource. The cover stories were about American energy independence. The promotional capital flowed to the producers.

Most of those equities ended the decade at a fraction of their peak. Chesapeake, once the second-largest natural gas producer in the United States, filed for Chapter 11 in 2020.

The value, in the meantime, accreted to the constrained midstream — the pipelines and gathering systems that couldn’t be built fast enough to move the resource to market. Companies like Enterprise Products Partners, Energy Transfer, Williams, Targa. Unglamorous toll roads, sitting on top of a flood, charging by the barrel.

The midstream was the choke point. The midstream got the multiple.

Semiconductors, 2014-2024.

On the surface, this was a story about chip designers — Nvidia, AMD, Intel, the rise of the fabless model. Beneath that surface, the single greatest compounding asset of the decade was a Dutch company called ASML, which makes the EUV lithography machines without which advanced chips simply cannot be manufactured.

ASML went from roughly €50 per share in 2014 to over €700 at its peak.

It did this by being, not the most exciting company in semiconductors, but the only company that could solve a constraint nobody else had figured out how to solve. There is, today, exactly one supplier of leading-edge EUV in the world.

That is a choke point made into an equity.

The 1970s nuclear cycle, the original one.

The reactor manufacturers — Westinghouse, General Electric, Combustion Engineering, Babcock & Wilcox — had a mixed decade. The companies that held the specialized forging capability for reactor pressure vessels (there were only a handful, globally) did considerably better, for considerably longer.

Three different industries. Three different decades. The same pattern, each time.

In a capacity-constrained build-out, the multiple expands at the choke point, not at the headline.

The reactor designers of the current wave are the headline.

The fuel cycle — and specifically enrichment and HALEU fabrication — is the choke point.

I don’t think this is a particularly subtle observation. I think it’s an observation the market hasn’t yet priced because the market is, as it often is, fascinated by the most visually compelling part of the story.

The visually compelling part of the story is a small modular reactor humming next to a data center in Texas in 2032.

The economically important part of the story is a Pentagon-sized building in Ohio, full of centrifuges spinning at supersonic speeds, between now and then.

The slow atoms.

VIII. Who sits on the choke point

A few names worth knowing, what each one actually does, and how I’d start to think about them.

I’m going to keep this section relatively high-level — enough to give you the map of the landscape, but I’m holding back the operational layer (sizing, entry levels, risk framework, scenario allocation, what I’m doing in my own book) for the deep-dive version, which I’ll point you to at the end of this letter.

Centrus Energy (NYSE: LEU)

The cleanest, most asymmetric expression of the trade.

Centrus operates the only first-of-a-kind HALEU production cascade in the United States. As of January 2026, the company holds a fresh $900 million DOE award, on top of a $3.7 billion sales backlog extending to 2040, on top of a private-capital base above $1.6 billion, on top of forward supply contracts with sophisticated international buyers including Korea Hydro & Nuclear Power.

The equity is volatile and the path is not without execution risk. Phase III of the HALEU contract has to deliver. The commercial centrifuge ramp has to scale. The funding stack — DOE awards, ATM equity, convertibles — is being assembled in real time.

But the question to ask about Centrus is not “will the next quarter be smooth.”

It is: “what does this asset look like in 2029, if Piketon is producing at commercial scale?”

My base case answer: significantly larger, and significantly re-rated.

Cameco (NYSE: CCJ)

The lower-volatility way to express the same thesis.

Cameco is, at the surface, a uranium miner. The more interesting story since November 2023 has been its 49% stake in Westinghouse — the legendary American nuclear company that emerged from bankruptcy in 2018, was acquired out of private ownership by Cameco and Brookfield Renewable in late 2023 at an enterprise value of approximately $8 billion, and now sits as one of the dominant Western fuel fabricators for the existing fleet.

In October 2025, the U.S. government, Brookfield, and Cameco announced a transformational partnership in which the U.S. government took a participation interest in Westinghouse. That interest is convertible — if Westinghouse IPOs at a valuation of $30 billion or above by January 2029 — into a warrant for 20% of the public value above $17.5 billion.

Read that twice.

The implied U.S. government view of Westinghouse’s potential equity value is meaningfully north of $17.5 billion. Cameco’s 49% of that, if the math plays out, is a number that does not yet appear in most sell-side models.

Sprott Physical Uranium Trust (TSX: U.UN)

The beta hedge.

Holds physical uranium pounds, correlates with spot price, useful as a way to get broad exposure to the cycle without single-name risk.

Watching brief: Urenco

Not currently public. The UK/Netherlands/Germany consortium structure is under increasing strain as enrichment demand outstrips capacity. Urenco’s New Mexico facility started production from a new centrifuge cascade in May 2025 — the first phase of a 700,000 SWU annual expansion finishing in 2027.

If a path to public exposure ever opens — IPO, partial monetization, structural change in the consortium — Urenco is, in my view, the single highest-quality enrichment asset in the West.

Not investable today. On my radar.

IX. What I don’t like

This is the section that, in my experience, separates research from marketing. So let me be specific.

The current SMR designer rally, at current prices.

Oklo at roughly $11 billion of market capitalization, pre-revenue, with no NRC-certified design, is not a price I’m willing to pay. Sam Altman as chairman is interesting; AI-adjacency is interesting; neither is a substitute for fuel availability or a regulatory approval.

NuScale, at about one-third of Oklo’s valuation and with an actually-certified design, looks more reasonable on a relative basis. But it still asks the investor to underwrite a long sequence of regulatory, construction, and fuel-availability outcomes, any of which can slip by years.

Some of these companies will succeed. I don’t know which ones.

I’d rather own the picks-and-shovels than guess the prospectors.

Pure-play junior miners with no producing assets.

A reasonable trade in 2020 at $20/lb uranium. A crowded, sentiment-driven trade at $80/lb. The marginal cost of new supply is materially below where the spot has traded in the last eighteen months, and new entrants will arrive. I prefer the constrained, slow-to-build segments of the cycle to the easy-to-add ones.

Anything that requires Russian fuel to find a workaround back into Western supply chains.

The U.S. ban is on. The 2028 waiver cliff is hard. The political momentum is going the other direction, not back. Structuring a thesis around a thaw is asymmetric in the wrong direction — modest upside if you’re right, severe downside if you’re wrong, regulatory tail you don’t want to wear.

X. How this trade could be wrong

I’d like to do something newsletters don’t tend to do, which is openly tell you how I could be wrong.

Scenario one: Western enrichment capacity comes online faster than I expect.

Centrus delivers Phase III on time and under budget. General Matter executes at Paducah. Orano’s Project IKE accelerates. Urenco’s New Mexico expansion completes ahead of schedule. In that world the bottleneck closes by 2028-2029, and the enrichment names trade flat-to-down 20-30% as the structural scarcity narrative fades.

This is the bear case. I rate it: possible, but unlikely on the timeline that matters. Greenfield enrichment plants do not, historically, come in early or under budget.

Scenario two: SMR deployment slows.

NRC approvals stretch out. Hyperscaler commitments soften as power-purchase economics get re-examined. Demand for HALEU specifically pushes from 2030 to 2035 or beyond.

In this world the basket still works on the LEU side — the existing reactor fleet still needs fuel — but the HALEU optionality embedded in Centrus compresses. Centrus trades more like a slow industrial. Cameco-Westinghouse continues to compound on the existing fleet. The trade is still positive, just smaller.

I rate this: meaningful probability.

Scenario three: A geopolitical shock pushes the bottleneck even harder than I expect.

Russian export controls. A second war. Sanctions tightening before the 2028 cliff. The basket re-rates more violently than my base case.

I don’t model this. But it is, structurally, the asymmetry — and it is why I sit in this trade with conviction.

XI. What I’m watching

— Centrus Phase III DOE milestones. The next material data point is the production-rate ramp through 2026. Watch the kilogram figures in 8-Ks.

— General Matter’s Paducah construction timeline. A stealth-mode startup with a $900 million federal commitment and a 100-acre lease on existing federal land is an unusual entity. Construction was expected to begin in 2026; operations by 2034. The first construction milestone will tell us a great deal about whether the U.S. build-out is going to compress or stretch.

— Spot UF₆ conversion pricing. Currently, in my view, the cleanest leading indicator for the broader cycle.

— Westinghouse IPO chatter. The U.S. government participation structure has a five-year fuse. If discussions begin in earnest, the implied valuation embedded in Cameco’s 49% stake becomes a topic the sell-side cannot ignore.

— Hyperscaler PPA-to-fuel disclosures. None of the announced SMR power purchase agreements has publicly disclosed a fuel supply plan. Watch for the first one. It will be a market-moving disclosure.

XII. Where this letter goes next

If you’ve read this far — thank you. Genuinely. That’s around five thousand words on uranium centrifuges, and the fact that you’re still here tells me something about the kind of reader Macro Notes is for.

The free version of this letter is, and will remain, free. I want as many people as possible reading the kind of long-form, first-principles work I’ve tried to do in this issue. That’s the deal.

But there’s a second layer of work that, for practical reasons, doesn’t fit inside a public letter — and that’s where the Founding Member tier comes in.

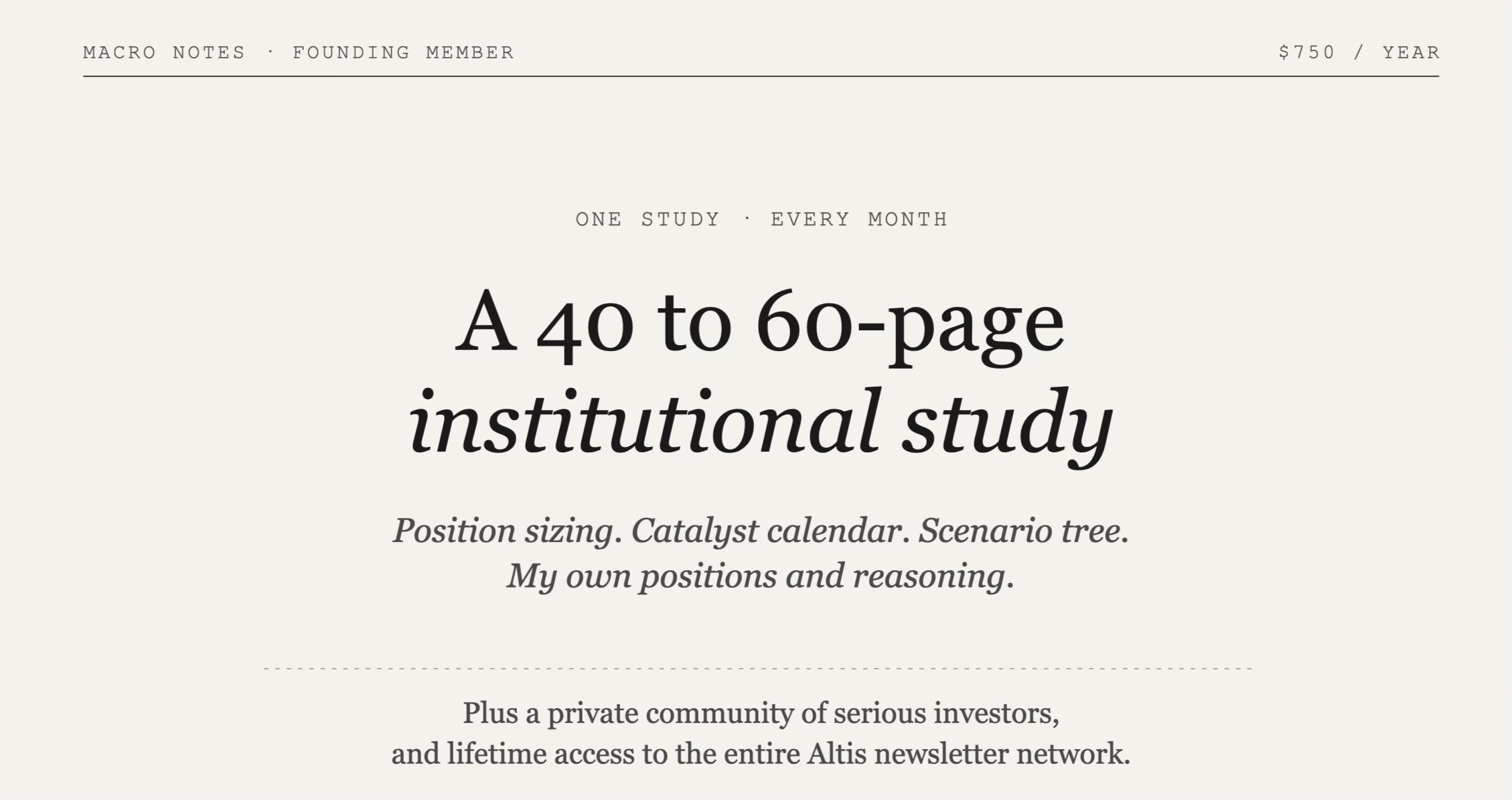

Macro Notes — Founding Member · $750 / year

This is for the reader who wants to go from understanding the thesis to operating against it. It’s built for serious investors — professional or retail — who want the deeper work, the closed conversation, and the network of publications I read alongside Macro Notes.

A short note on the price before I walk through what’s inside: the Founding Member rate moves up regularly as the work and the network grow. The price you lock in today is the price you keep, for as long as you stay. It will not increase on you. If you’ve been thinking about it, joining sooner rather than later is the rational move.

Here’s what you get.

One full deep-dive thesis, every month.

This is not a longer version of what you just read. It’s a different object entirely.

What you just finished is the map — the why, the how, the historical pattern, the names worth knowing. The monthly Founding Member deep-dive is the operating manual — a 40-to-60-page institutional-grade study designed to let you actually restructure a meaningful part of your portfolio around the thesis, with confidence, and with a clear framework for what to do as the situation evolves.

A typical deep-dive includes:

— A complete operational layer on the thesis. Position sizing across different investor profiles. Multiple ways to express the trade depending on your risk tolerance and time horizon — concentrated single names, sector basket, options expression, levered vs. unlevered, public-market vs. private-market adjacencies. The exact entry and exit framework I’m using, with the price levels and triggers that matter.

— A full catalyst calendar. Twelve to twenty-four months of dated events that will move the thesis — earnings, regulatory milestones, contract announcements, geopolitical inflection points — with my view on what each catalyst means and how to position into it.

— Portfolio integration framework. How this thesis interacts with the rest of a serious portfolio. What it correlates with. What it hedges. What it duplicates. Sizing guidance for someone allocating 1%, 5%, or 15% of their book to it. The institutional-grade work most retail readers never see — because most retail letters never do it.

— A full scenario tree with probability-weighted outcomes. Not just “bull / base / bear” — a structured map of how the thesis evolves under three to five distinct macro environments, and how the basket repositions in each.

— What I’m actually doing in my own portfolio, and why. Specific positions, sizing, entry levels, what I’m adding to, what I’m trimming, and the reasoning behind each move — updated in real time through the community as the situation changes.

— Companion data. The underlying models, the source documents I built the thesis on, the spreadsheets where I size the basket. Built so you can replicate, challenge, or extend the work yourself rather than take it on faith.

The slow-atom problem is the first of these — and the full Founding Member version of it goes considerably further than the letter you just read.

It maps the entire $200 billion build-out across enrichment, conversion, fabrication, and transport. It identifies the eight to twelve specific equities I think compound through this decade — only three of which appeared in this free issue. It lays out how I’m sizing them in my own book and at what levels I add or trim.

And it builds out the second-order and third-order trades that sit downstream: the specialty alloy producers, the centrifuge component suppliers, the transport-cask manufacturers, the obscure utility names that have quietly become enrichment offtake buyers.

It is, in other words, the difference between being convinced and being positioned.

The next deep-dive is already in the works.

Private Telegram community.

A closed group of Founding Members — operators, allocators, analysts, and serious individual investors — where we share ideas, debate theses, and react to the news as it happens.

This is the part of the experience that, in my view, ends up being the most valuable over time. The deep-dive gives you the work.

The community gives you the network. Most of the readers I’ve spoken to who’ve been in similar communities for a year or more tell me the same thing — the network ends up paying for the subscription many times over, often through a single idea, conversation, or introduction that wouldn’t have happened anywhere else.

Direct access.

Founding Members get the channel where I actually answer questions on positions and theses I cover. Not at the speed of a full advisory practice — but in a way no free reader gets. If you’re stuck on a sizing question, a thesis you don’t fully buy, or a catalyst you want my read on, you can ask, and I’ll answer.

Lifetime Premium access to the Altis newsletter network.

This is the part I’m most pleased to be able to offer, because the aggregate value here is real — several thousand dollars a year of subscriptions, included for as long as Macro Notes exists, and yours to keep even if you ever choose to leave Macro Notes itself.

— Macro Notes — Deep macro research, structural investment theses, and specific equity/commodity/credit positions. The flagship.

— Public Markets — Institutional-grade equity analysis. Earnings forensics, valuation frameworks, sector rotations.

— Private Markets — Private credit, PE, and alternative assets. What’s moving in the $2T shadow banking system.

— Future Digest — Tech-meets-investing deep dives. AI infrastructure, energy transition, and the sectors shaping the next decade.

— Next Financial — Supply-chain intelligence. The Tier 2 and Tier 3 companies nobody’s watching yet.

— Solo Capitalist — High-conviction, concentrated investing. Real portfolio, real entries, full transparency.

— Tech Economist — The economics of tech, stripped of hype. Unit economics, TAM reality checks, structural analysis. — Every new newsletter we launch, acquire, or partner with — automatically included, at no extra cost. Forever.

The shape of it

For $750 a year — you get:

— Twelve full operational deep-dives per year, any one of which can pay for the subscription several times over if a single thesis works

— A permanent seat in a private community of serious investors

— Direct access to me on the work

— Lifetime Premium across the entire Altis network, worth several thousand dollars on its own

— and yours to keep, forever, even if you ever leave

The Founding Member tier is, deliberately, not for everyone. The free version of Macro Notes will keep doing what it does — long-form, first-principles essays on the structural setups I find most interesting. If that’s what you want, you’re already in the right place.

But if you want the deeper version — the one with the operating manual, the closed conversation, and a permanent seat in the network — that’s what $750 a year buys, at today’s rate.

XIII. One last thought

The slow atoms are not glamorous. They will not appear on a quarterly investor letter cover. They will not make for a compelling product launch.

They will, however, in my view, be among the assets that compound through this decade — while the equity market spends another eighteen months staring at the wrong room.

If you got something out of this — share it with one person you think would, too. That’s how this kind of project grows.

And if you didn’t — write back and tell me why. I mean that.

The next free issue, in two weeks, looks at the second-order trade in GLP-1s: not who wins from Ozempic, but who inherits the roughly $200 billion that is slowly walking off the plate of global food, snack, and discretionary alcohol consumption. It is, in its own way, also a story about constraints that have not yet been priced.

Until then.

— Pierre

Thank you for clarification on a lot of misinformation&confusion ♥️

@Dawn Run Intelligence dawn you might enjoy this

Damn! Now this is how to write an articulate explainer. Bravo. I will be summarizing this into a shorter version with some other commentary for my own Substack page called Meanderings. You will be duly accredited and recommended.