The Embodied AI Inflection: When Physical Intelligence Meets Human Labor

The AI revolution has transformed what we can know and decide. It has not yet transformed what we can build and move.

In factories, warehouses, and logistics networks across the developed world, the same constraint keeps reappearing: there simply aren’t enough reliable human hands to meet demand. Labor shortages in manufacturing and logistics have become structural. At the same time, governments are spending hundreds of billions to reshore critical production. The missing piece is no longer intelligence — it is physical execution at scale.

In 2026, that gap is finally closing. Humanoid robots and other embodied AI systems are moving from controlled demonstrations to paid, productive work on real factory floors. This is not another incremental improvement in industrial automation. It is the emergence of general-purpose physical intelligence that can adapt to human environments without requiring those environments to be completely redesigned.

What Embodied AI Actually Means

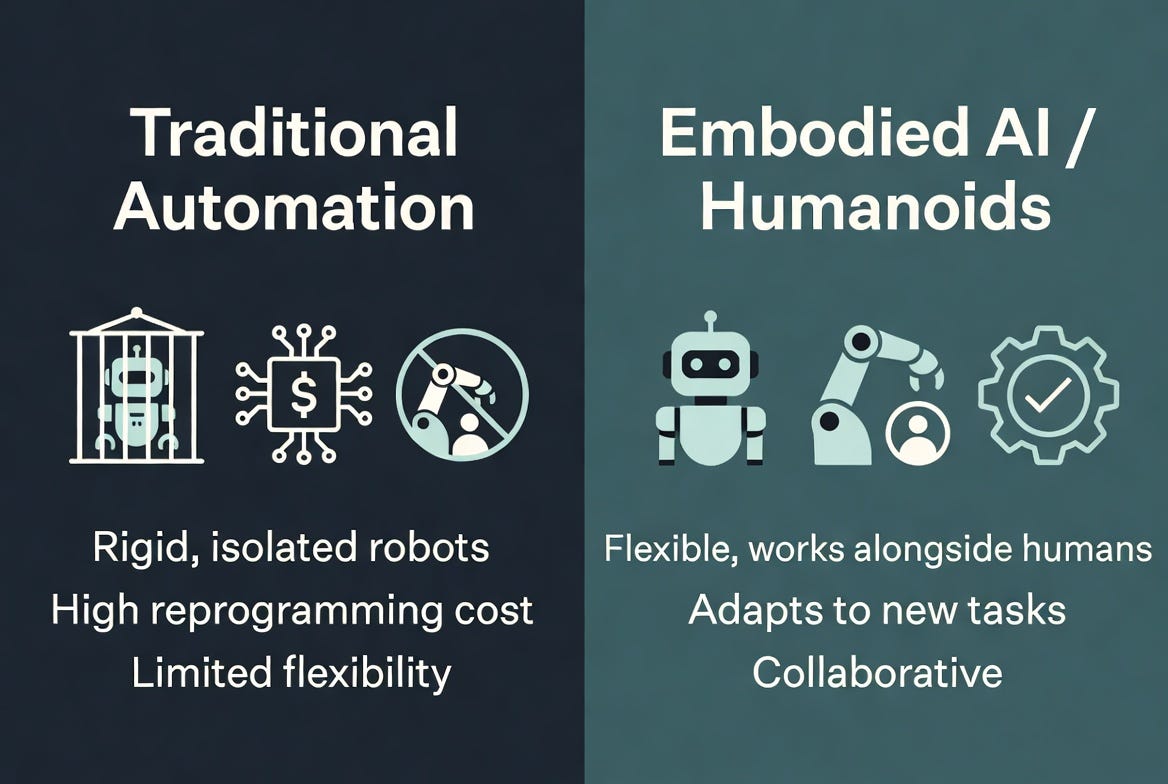

Embodied AI refers to artificial intelligence systems that possess a physical body capable of sensing, reasoning, and acting in unstructured real-world settings. The humanoid form factor holds a decisive advantage: our factories, tools, vehicles, and buildings were all designed for human proportions and capabilities. A robot that can use the same doors, stairs, workstations, and hand tools as a person can be deployed with far less modification to existing infrastructure.

The technological stack has three critical layers:

Hardware — high-performance actuators, sensors, and batteries that deliver human-like dexterity and endurance

Intelligence — foundation models that translate vision and language into coherent physical actions

Integration — the ability to operate safely and usefully alongside human workers rather than in isolated cages

The decisive shift occurring right now is the move from “can the robot perform a scripted task in a lab?” to “can it reliably contribute to output on a live production line for full shifts?”

The 2026 Inflection Point

The global humanoid robot market is currently valued at roughly $4–5 billion. Most credible forecasts see it reaching $15–30+ billion by 2030–2032 as volumes scale and unit economics improve. But the more important signal is not the market size projection — it is what is already happening on the ground.

Consider the most advanced real-world deployment to date:

At BMW’s Spartanburg plant in South Carolina, Figure AI’s humanoid robots worked 10-hour shifts, five days a week, for over ten months on an active automotive assembly line. They handled more than 90,000 parts and contributed to the production of over 30,000 BMW X3 vehicles, achieving placement accuracy above 99%. BMW has since expanded the program to its Leipzig facility in Germany. This is no longer a pilot in the traditional sense — it is contracted, paid, productive work.

Tesla continues to ramp Optimus units inside its own Gigafactories, focusing on repetitive internal tasks while preparing for external deployments. Boston Dynamics has shifted its new all-electric Atlas platform toward industrial deployments, with initial fleets already allocated to Hyundai’s advanced manufacturing sites. Agility Robotics’ Digit platform is now operating in multiple Amazon and third-party fulfillment centers.

These are not isolated experiments. They represent the first concrete proof that general-purpose humanoid platforms can deliver measurable value in complex, human-centric environments.

Early connections to brain-computer interface technology are also appearing. Neuralink patients have already demonstrated direct thought control of robotic arms for practical daily tasks. This points toward future hybrid architectures in which humans can supervise or directly teleoperate fleets of embodied systems at a cognitive level.

Why This Matters Now

Digital AI created an explosion of productivity in information work. Embodied AI is the necessary counterpart for the physical economy. Without it, reshoring initiatives will continue to be constrained by labor availability, and the full productivity gains from AI will remain bottlenecked at the last mile of physical execution.

The first wave is industrial augmentation — robots working alongside humans in structured but still variable environments. The second wave, already visible in pilot planning, extends into logistics, construction, defense support, and eventually eldercare and domestic assistance.

The companies that master the combination of hardware reliability, scalable AI training, and real-world deployment data will define the next major platform layer of the economy.

This free section provides the context, verified mid-2026 operational developments, and the strategic rationale for paying attention to this theme now.

For paid MacroNotes subscribers (full analysis unlocked immediately below):

We deliver the deeper investor analysis:

Head-to-head comparison of the leading embodied AI platforms and their technological moats (Figure AI, Tesla Optimus, Boston Dynamics Electric Atlas, Agility Robotics, and key challengers)

Current valuation context, funding dynamics, and realistic routes for public and private market exposure

Portfolio construction framework, including allocation sizing, timing considerations, and risk management specific to this emerging theme

Detailed catalyst calendar through 2027–2028 (production scale-up milestones, new commercial contracts, technical breakthroughs, and regulatory developments)

Comprehensive risk assessment covering technical execution, unit economics, safety and liability, labor market disruption, competitive intensity from Asia, and capital requirements

Downloadable tracker covering active deployments, pilot results, unit economics indicators, and companies to monitor

The physical world is finally becoming addressable by general-purpose intelligence. The implications for productivity, manufacturing strategy, and labor markets are profound — and the companies positioned to lead are already revealing themselves through real deployments rather than promises.

Macro Notes Premium - The Embodied AI Investment Map