The Right Thesis

The way I invest, and the way Macro Notes works, is to always seek to build theses first and foremost.

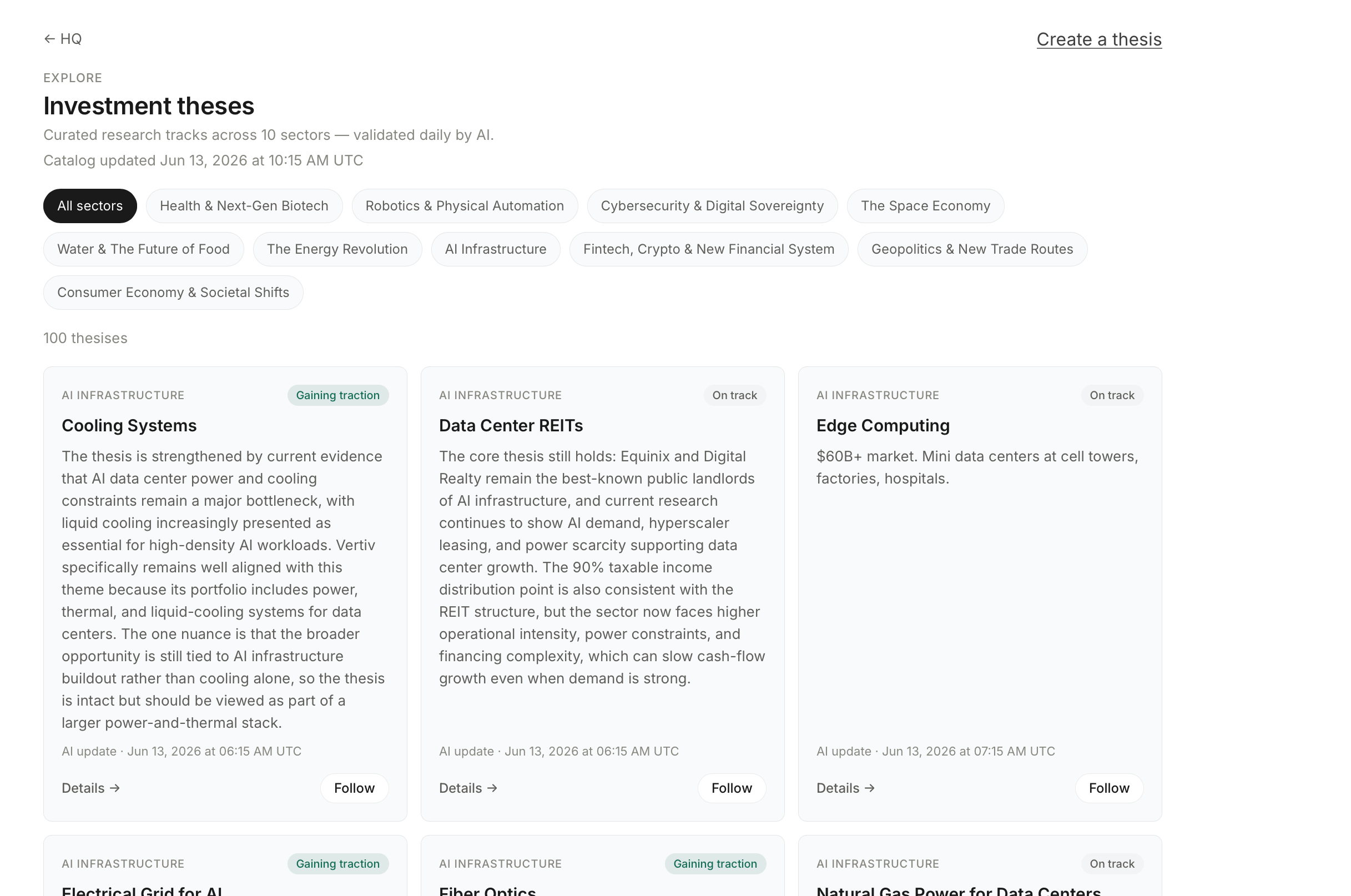

A few months ago, I developed an in-house AI agent that tracks more than 100 investment theses.

Some are occasionally removed, new theses are added, all while monitoring the markets and taking into account every event that either strengthens a thesis or makes it less compelling.

The reality is that a thesis is never entirely correct—it’s more accurately a hypothesis. But you can readily assign it a probability of success based on all the information available, as well as on the information that’s missing.

And for this kind of work, AI is extremely effective.

Each thesis is analyzed in real time: new theses are generated, and some are occasionally invalidated. The agent also proposes a selection of companies to position yourself on a given thesis (long or short)—not as a recommendation, but simply to show which companies are exposed to it.

Here’s what the interface looks like:

In a month, I’ll be opening up this AI agent for free to every Premium member of Macro Notes—and I think it may be the single best piece of value we’ve ever put on the table.

Here’s why.

When you invest, the whole game comes down to one thing: being right often enough that your portfolio stays in the green. Over the short term, that’s genuinely hard—too much noise, too much randomness. Over the medium to long term (which is where I operate), it becomes far more achievable.

But only on one condition: that you truly understand what you’re buying. The company itself, yes—but also its market: who its customers are, how fast that market is growing, and how the financial markets are likely to value it.

Because here’s the subtlety most people miss: a company can be barely profitable, post thoroughly unremarkable revenue, and still see its stock climb—simply because the market is pricing in the future, not the present. What you’re buying is rarely what the company is today. It’s what investors collectively believe it will become.

10 Theses I’m Tracking Right Now

There’s one thing it took me a long time to accept as an investor: you don’t invest in a market, a product, or a company. You invest in a story. The company is just a character. The thesis is the plot — the one that builds, that collapses, that gets bought out in the third act.

The best example landed on a trading screen yesterday. SpaceX went public, and the market handed it a valuation north of $1.7 trillion — the largest IPO in history.

The SpaceX thesis is the space market: the company that opens it, that operates it, and that will spin off the dozens of products built on top — Starlink internet reaching every corner of the planet, data centers in orbit, solar power generated in space, resource extraction off other worlds, eventually colonies on the Moon or Mars. Musk isn’t selling a rocket.

He’s selling that story. Just as he sold the story of the electric car for Tesla — and everyone who shorted Tesla on its very real negative signals learned the hard way what happens when the story is right and plays out anyway. A correct thesis can carry an investment even when the noise around it screams sell.

That’s the whole game. Be right about the story, and the rest tends to follow.

Here are ten of those stories, as the agent displays them. They cluster around four great currents: rearmament, AI’s hunger for power, the obesity-drug revolution, and robots finally taking on a body….

I’m opening one in full. The other nine are reserved for Premium members.

I. Rearmament

Thesis 01 — The NATO rearmament supercycle is structural, not cyclical

Estimated probability of success: 84%

Picture an ocean liner changing course. It doesn’t turn on a dime — but once it’s locked onto its new heading, nothing stops it for years. That’s exactly what happened in Europe between 2022 and 2025. The heading changed, and the commitments now reach well beyond the next news cycle.

The thesis isn’t “defense stocks go up.” It’s deeper: the budgets being committed are stretching order books into the 2030s. At the 2025 Hague Summit, allies pledged to spend 5% of GDP on defense and security by 2035. The European Union announced a plan capable of mobilizing up to €800 billion by 2030. Germany alone is raising its military budget from €86 billion in 2025 to €108 billion in 2026, with up to €400 billion in additional borrowing planned over five years. And for the first time in the Alliance’s history, all 32 members crossed the 2%-of-GDP threshold in 2025.

And yet the caveat is everything — and this is where the agent earned its keep this quarter. A large part of the rally is already in the price. Rheinmetall has climbed roughly 900% in three years. When a stock has run that far, it becomes hypersensitive to the smallest disappointment. We watched it happen live: the stock traded around €1,256 in early June 2026, down about 21% year-to-date and 33% over twelve months, after a soft quarter. The other, more brutal risk would be a ceasefire in Ukraine: it could turn market sentiment even if the budgets themselves don’t budge.

But here’s what makes the story interesting: while the stock corrected, the thesis itself strengthened. Rheinmetall’s order backlog reached €73 billion at the end of March 2026, including €5.5 billion from its newly consolidated naval business for the first time. The company confirmed its target of €14–14.5 billion in revenue for 2026, at roughly 19% operating margin. On May 28, Ukraine’s parliament ratified a €90 billion European loan, partly earmarked for defense-industrial capacity. And management still targets some €50 billion in sales and over 20% margin by 2030.

This is the perfect textbook case: the thesis and the trade diverge. The underlying story stays intact; the stock takes a breath. The agent tracks both separately, because confusing the two is the most expensive mistake an investor can make.

Exposed companies (illustrative, not a recommendation) Rheinmetall, BAE Systems, Thales, Leonardo, Saab. Note: BAE is the only name in the group with meaningful exposure to the U.S. Pentagon (~45% of revenue), which makes it a differently-shaped bet than the European pure-plays.